The Importance of Business Insurance for Medical Professionals

Debt Protection

Debt protection insurance is designed to ensure that a practice remains financially stable if an owner dies or is unable to work due to illness or disability. The policy provides a lump sum that can be used to settle outstanding debts, helping to maintain operational continuity and reassure customers and suppliers. It can also relieve personal guarantees tied to assets such as a family home, ensuring that the remaining business owners are not personally liable.

This type of insurance is generally treated as capital in nature, with proceeds typically income tax free, although capital gains tax may apply.

Revenue Protection

The loss of a key individual, such as a partner or senior employee, can significantly impact the practice’s profitability, operational capacity, and reputation. Key person insurance helps mitigate this risk by providing the business with a financial infusion in the event of the death, disability, or illness of a critical individual. The insurance can be used to cover the costs of hiring temporary staff, training new employees, or compensating for the loss in revenue, which helps to preserve the practice’s financial standing and continuity.

Ownership Protection

In the event of a partner’s death or incapacity, a buy/sell agreement ensures a smooth transition of business ownership. Such agreements outline how the practice will be valued, who will purchase the departing partner’s share, and the method of funding—often through insurance policies.

To ensure proper implementation, business owners will often need to consult with financial, tax, and legal professionals.

The tax implications of the premiums and proceeds from these policies depend on the funding structure and ownership of the insurance.

Operating as a Sole Practitioner?

For sole practitioners or small practices, business expenses insurance provides critical protection if the owner becomes temporarily incapacitated.

This coverage helps ensure that the practice continues to meet its financial obligations—such as rent, utilities, and staff salaries—during periods when the owner is unable to work due to illness or injury.

If the practice must be sold due to the owner’s prolonged incapacity, business expense insurance can help maintain the practice’s value until a sale occurs. Premiums for this type of insurance are generally tax-deductible, and claim proceeds are typically taxed in alignment with the expenses covered.

Cyber Risk Protection

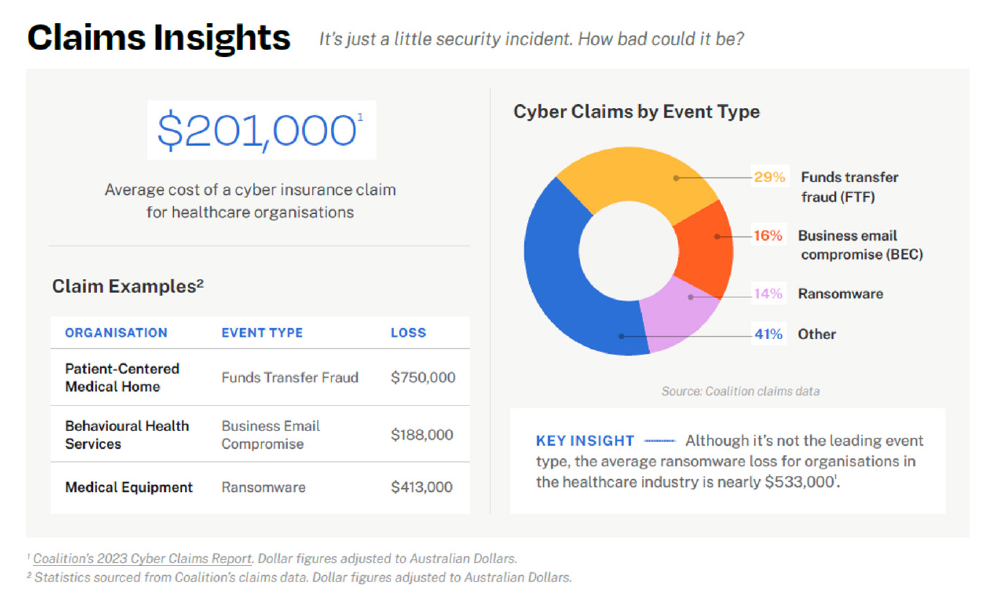

Given the increasing reliance on digital systems, protecting patient confidentiality is of paramount and increasing importance within the healthcare sector. Healthcare providers manage large volumes of sensitive data, including medical, financial, and personal information, which is frequently transmitted and stored digitally. As a result, healthcare practices are prime targets for cyberattacks.

The integration of technologies such as internet-connected medical devices, telemedicine tools, and remote monitoring systems adds complexity to the risk profile of healthcare providers. A breach or

disruption in these systems can have far-reaching consequences, potentially compromising patient safety and the continuity of care. At AMA, our team of experts can assist in managing and mitigating digital risks, ensuring that your practice is well-prepared to address and prevent cybersecurity incidents.

Planning for Long-Term Security

Whether operating in a partnership or as a sole practitioner, securing the appropriate insurance coverage is essential for the continued success of your medical practice. At AMA, we offer expert guidance in developing comprehensive business protection plans to ensure a seamless transition and provide peace of mind in the event of unforeseen circumstances. Safeguard both your personal and professional interests to ensure the long-term sustainability and stability of your practice.